The Polite Surrender

How Europe’s regulatory instinct became its most elegant self-inflicted wound

Europe generates enough savings to fund its own future. It simply cannot deploy them at home. The result is a continent that finances American growth, Chinese industrial strategy, and Gulf sovereign wealth — while watching its most promising companies relocate to jurisdictions that can back them. This is not a story about reckless banks or reckless deregulators. It is a story about a regulatory culture so focused on preventing the last crisis that it may be enabling the next one: the slow, polite surrender of European strategic capacity, one missed investment at a time.

By Mika Horelli, Brussels

There is a peculiar kind of genius in building a cage so sophisticated that no one inside it quite realises they are confined. Europe has been quietly perfecting this art for decades.

I was reminded yesterday in Brussels, sitting in a conference room listening to Enrico Letta, former Italian prime minister and author of the authoritative 2024 single market report, Much More Than a Market, offer his first reactions to a new study commissioned by the European Banking Federation. The study, produced by Oliver Wyman, arrived with a number that deserves to be tattooed somewhere prominent in every European finance ministry: 1.4 trillion euros.

That is Europe’s estimated annual investment gap. Not the deficit of some struggling peripheral economy. The shortfall of the entire continent, measured against what Europe actually needs to invest every year to remain competitive, resilient, and capable of shaping its own future.

For context, this figure has already grown considerably from the 0.8 trillion-euro estimate published in Mario Draghi’s landmark competitiveness report just a year ago. In twelve months, the chasm has not narrowed. It has widened by more than half a trillion euros.

And yet, in the fine tradition of European institutional gatherings, the mood in the room was earnest rather than alarmed. There were PowerPoint slides. There were panel discussions. There was excellent coffee, wine and beer.

Outside, the world continued not waiting.

Letta said something that stayed with me long after the event had ended. He did not want Europe to become a colony, not of the United States, not of China. He wanted Europeans to be Europeans. He was not speaking at an anti-globalisation rally or channelling some romantic vision of a European superstate. He was talking about capital markets. About the unfinished architecture of the single market. About the gap between Europe’s savings and Europe’s investments.

He chose the word colony anyway.

It is worth pausing on that word. In the twenty-first century, colonies do not typically arrive by gunboat or through formal annexation. They emerge through dependence. Dependence on foreign technology platforms. Dependence on foreign capital markets. Dependence on security guarantees underwritten elsewhere. Dependence on decisions made in boardrooms and legislatures where European preferences are noted, acknowledged, and then politely disregarded.

Letta is not alone in reaching this conclusion. Mario Draghi reached the same destination from the angle of industrial competitiveness. The former president of Finland, Sauli Niinistö, arrived there from a security and resilience perspective. Three statesmen, three reports, three different starting points, one diagnosis: Europe does not suffer from a lack of analysis. It suffers from a shortage of political courage to act on what the analysis reveals.

The Oliver Wyman report placed a specific, somewhat uncomfortable stress test on one part of that diagnosis: the role of European banks.

The argument, in essence, is this. Europe’s future investment needs are not simply large; they are structurally different from the investments Europe has financed over the past generation. They are long-duration. They are capital-intensive. They carry higher risk profiles. Green infrastructure. Defence logistics. Digital transformation. Biotechnology. These are not the kind of assets that lend themselves to short-term, risk-averse balance sheet management. These are precisely the assets that patient, well-capitalised European banks ought to be well positioned to finance — and that European banks are currently constrained from financing by a cumulative architecture of regulation that, taken individually, makes perfect sense, and taken collectively, makes rather less of it.

Here is where the story becomes genuinely interesting, and where a journalist who has spent too many years watching European institutions confuse procedural virtue with strategic effectiveness starts to feel a familiar unease.

Since the 2008 financial crisis, European banking regulation has been pursued largely in the spirit of “never again”. The reasoning was sound. Banks had been reckless. Taxpayers had paid the consequences. Capital requirements needed strengthening. Supervisory oversight needed tightening. Risk needed to be taken more seriously. All of this was correct.

The implementation, however, has followed a pattern recognisably European in its thoroughness, good intentions, and unintended side effects.

Layer by layer, capital requirement by capital requirement, reporting obligation by reporting obligation, supervisory burden by supervisory burden, European banks have been made progressively more resistant to the thing regulators most wanted to prevent — and simultaneously less capable of doing the thing Europe most urgently needs them to do.

The Oliver Wyman study makes this point with the blunt force of data rather than opinion. European banks are well-capitalised. European banks are resilient. European banks are safe in precisely the way post-crisis regulation intended. They are also, as a direct consequence of this architecture, less able to deploy capital into the long-duration, higher-risk investments that Europe’s future requires.

This is what it looks like when you throw the baby out with the bathwater — not all at once, dramatically, but incrementally, over fifteen years, one sensible piece of legislation at a time.

A fair-minded reader will object at this point, and the objection deserves a direct answer. The Oliver Wyman report was commissioned by the European Banking Federation, which is, to put it plainly, a lobbying organisation for European banks.

Self-assessments of regulatory burden by those being regulated are rarely exercises in disinterested analysis. And European banks have, it should be noted, been performing rather well of late. The year 2025 was historically strong for the sector; interest margins remained elevated, merger and acquisition activity was robust, and major institutions posted capital ratios comfortably above regulatory minimums. If the cage is so constraining, the birds appear to be singing.

These are legitimate points. But they do not quite reach the heart of the matter.

The question is not whether European banks are profitable today. The question is whether European capital markets, banks and non-banks together, the full financing continuum, are structurally equipped to deploy European savings into European investment at the scale and risk profile required by Europe’s strategic situation. On that question, the evidence from sources considerably less interested than the EBF is unambiguous: they are not. The European Investment Bank, the European Commission’s own Capital Markets Union assessments, and independent academic research all arrive at the same uncomfortable conclusion. The problem is real; it predates the Oliver Wyman report; and it will outlast it.

What the banking federation’s involvement usefully reminds us, however, is that deregulation is not the answer. The Silicon Valley Bank collapse in 2023 offered a brisk tutorial on what happens when the post-crisis regulatory architecture is dismantled prematurely, and European policymakers would be unwise to mistake a financing gap for a licence to abandon the prudential framework that has made European banks genuinely stable. The goal is not to return to 2007. The goal is to design a regulatory framework that treats resilience and productive investment as complementary objectives rather than competing ones.

There is a broader pattern here that transcends banking regulation, and it is the pattern that Letta’s word colony points toward.

Europe’s characteristic political failure is not, as its critics from the Anglo-American right like to claim, excessive integration. The failure is partial integration: enough cooperation to create interdependencies, but not enough to achieve the scale, capital depth, or strategic coherence needed to compete with actors who are not interested in Europe’s regulatory philosophy.

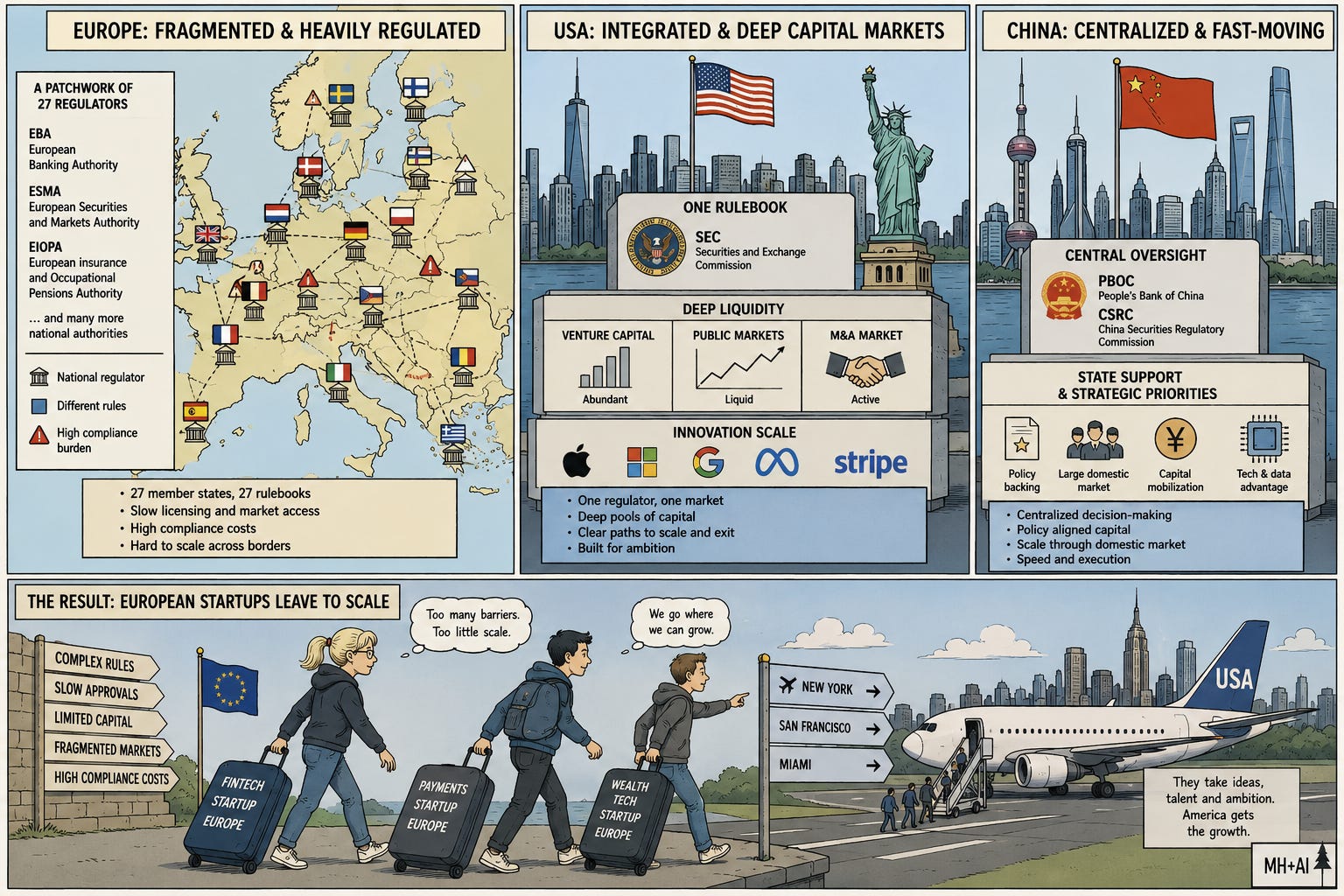

Consider what European financial fragmentation actually means in practice. A European start-up that grows to a certain size faces a choice: it can attempt to raise the capital it needs from a patchwork of national banking systems operating under overlapping but not identical regulatory regimes, from venture capital markets that remain dramatically undersized compared to their American equivalents, or from a European public capital market that is, to put it diplomatically, not yet the unified thing the Treaties suggested it might become. Or it can move. List in New York. Relocate its treasury operations. Gradually shift its strategic centre of gravity toward a jurisdiction that offers the depth of capital market it requires.

Many of them move. The European Investment Bank has documented this in detail. Between 2008 and 2021, roughly 30% of European unicorns relocated their headquarters, predominantly to the United States. At the scale-up phase, the critical moment when a promising start-up needs to grow into a serious competitor, European venture capital investment is below 10 per cent of the equivalent American figure. In more than four out of five European scale-up funding rounds, the lead investor is foreign.

This is not a metaphorical drain. It is a measurable, recurring, structurally predictable transfer of European innovation — and of European future tax revenue and employment — to jurisdictions outside Europe. The investment gap does not exist in a vacuum. It is being filled. Simply not by European capital, for European purposes, under European governance.

What fills it instead? American private equity. Sovereign wealth funds from the Gulf. Strategic investments from Asia. Each of these is a perfectly rational actor pursuing its own interests. None of them is pursuing Europe’s.

I am aware that this argument can sound like a brief for deregulation, and I want to be precise about why it is not.

The problem with European banking regulation is not that it exists; it is that it fails. The problem is that it was implicitly designed around a single objective, preventing the recurrence of 2008, and that objective, worthy as it was, has crowded out a second objective that was always present but less politically urgent at the time: ensuring that European banks could finance European growth.

These objectives are not inherently in conflict. A well-regulated, well-capitalised banking sector, one capable of providing long-duration, higher-risk financing to strategic industries, is not a mutually exclusive state. Other major economies have managed to pursue both simultaneously. The United States did not dismantle its post-crisis regulatory architecture; it calibrated it, debated it, pushed back on parts of it, and retained enough policy flexibility to adjust when the investment climate required.

Europe, by contrast, has tended to treat the Basel frameworks and their European regulatory transpositions as closer to moral commitments than to policy choices. Prudence became an end in itself. Safety became a synonym for virtue. And in the process, the question of what the banking system was actually for — the financing of productive economic activity, the intermediation of European savings into European investment, the support of European companies competing globally — receded into the background.

The Oliver Wyman report’s seven recommendations for enabling banks to play a larger role in financing European growth are, in this context, less a set of radical proposals than a gentle reminder that policy can be rebalanced without being abandoned. Better capital allocation frameworks. Reduced regulatory duplication across national jurisdictions. A more appropriate risk appetite, one that distinguishes between the kind of risk that caused 2008 and the kind of risk that is inherent in any long-term productive investment.

None of this is revolutionary. All of it requires political will that has, thus far, proved elusive.

It also requires honesty from the banking sector itself. If European banks want a seat at the table in the conversation about Europe’s strategic financing needs, they will need to demonstrate that the capital unlocked by regulatory recalibration flows toward the long-duration, higher-risk investments Europe actually requires; green infrastructure, defence logistics, deep technology rather than toward higher dividends, share buybacks, and the kind of short-term yield optimisation that regulatory relief historically tends to produce when left to its own devices. The argument for reform is strong. The argument for trusting that reform will automatically produce the desired outcomes is rather weaker.

Letta’s use of the word colony deserves one more moment of attention because it contains an insight that is easy to miss if you are accustomed to the European political discussion’s tendency to frame every question as a choice between integration and sovereignty.

The insight is this: the choice is not between integration and sovereignty. The choice is between different kinds of dependency.

A Europe that refuses to pool its capital markets, that maintains national banking systems with overlapping but incompatible regulatory frameworks, that watches its most dynamic companies relocate for lack of financing depth, that allows its annual investment gap to grow from 0.8 to 1.4 trillion euros in a single year — that Europe is not preserving its sovereignty. It is negotiating the gradual surrender of its capacity to act independently, one missed investment opportunity at a time.

The paradox, and it is genuinely a paradox, is that those who most loudly champion national financial independence — who resist the Banking Union’s completion, who block the Capital Markets Union’s consolidation, who defend national regulatory prerogatives against European harmonisation — are, in effect, defending the conditions under which European savings are deployed elsewhere, European companies are capitalised from elsewhere, and European strategic choices are constrained by dependencies created elsewhere.

They believe they are defending independence. They may instead be administering its slow dissolution.

There is a scene I keep returning to from the Brussels conference room.

The Oliver Wyman analysts presented their numbers with the measured professionalism of people who have spent considerable time with data that they know will be received politely and acted upon slowly. The audience of bankers, regulators, and policy professionals nodded with the measured engagement of those who have heard this argument before and are not entirely sure what the next step should be.

Letta spoke with the slightly weary authority of a man who wrote a significant report on European single market reform two years ago and is watching the world outside accelerate while the implementation of his recommendations proceeds at the pace of a particularly cautious committee.

Somewhere between the numbers, the nodding, and the excellent coffee, the 1.4 trillion-euro gap persisted. Donald Trump’s second presidency continued to pursue its logic of transactional great-power competition. China continued its long-term industrial strategy with the patient confidence of a civilisation that is accustomed to thinking in decades rather than electoral cycles.

Neither Washington nor Beijing was in the room. Neither needed to be. Their interests were adequately represented by the investment gap itself and by the capital that European savings generate, which European markets, in their current configuration, are insufficiently equipped to deploy at home.

The remarkable thing about this moment — and Letta, Draghi, and Niinistö have all said some version of this — is that Europe is not being defeated by superior competitors. It is being outpaced, in significant part, by its own institutional preferences.

European regulators are not corrupt. European policymakers are not foolish. European capitals do not lack talented, serious people who understand perfectly well what the numbers mean. The European Banking Federation did not commission a study from Oliver Wyman because anyone needed to be told that a 1.4 trillion euro investment gap is a problem.

The problem is the gap between diagnosis and action. The problem is that the political economy of European reform consistently rewards those who defend existing arrangements over those who propose changing them. The problem is that the national politics of every member state generates incentives to protect domestic financial champions, preserve national regulatory prerogatives, and avoid the difficult conversation with voters about what it actually means to share sovereignty to preserve it.

The problem, in short, is not analytical. It is political.

Europe does not lack prescriptions. It lacks the courage to take the medicine, or, more precisely, lacks the political architecture that would make taking the medicine in the interest of those who would have to administer it. And it lacks, perhaps above all, the institutional capacity to ensure that when the medicine is finally administered, it actually treats the patient rather than simply enriching the pharmacist.

A colony, Letta suggested, is not necessarily a place that has been conquered. It is a place that has been made dependent.

The risk Europe faces is not dramatic. It will not arrive with flags and declarations. It will arrive, if it arrives, through the accumulated weight of investment gaps, regulatory constraints, and financing shortfalls; through the steady migration of European ambition toward jurisdictions better equipped to finance it; through the gradual erosion of European capacity to act strategically at the moments when strategic action is most required.

Europe can still change course. The analysis is clear, the prescriptions are available, and the window for choosing a different trajectory has not yet closed.

But the coffee at these events is always very good, and the meetings are always very cordial. The gap between diagnosis and action has been widening for longer than anyone in that Brussels conference room would be entirely comfortable admitting.

The question is not whether Europe knows what needs to be done. The question is whether knowing is enough. History, on this particular point, is not especially encouraging.

Mika Horelli is a Finnish freelance journalist based in Brussels. He has covered economics and European affairs from Copenhagen, New York, and — for the past nine years — Brussels.